- Road To Carry Newsletter

- Posts

- 🎓PE Training: Continuation Funds

🎓PE Training: Continuation Funds

History, structure, and economics of continuation funds

Dear readers, I’m trying out a new content format for Tuesdays, focusing more on educational and training content. I’d love to hear your thoughts—please share your feedback via the poll at the end of this post!

What’s Topical: Continuation Funds

Secondary Market ($ in billions); Source: Evercore, GCM Grosvenor

2024 marked a landmark year for continuation funds, with transaction volumes rising to over $70 billion. Some of the largest deals in the last few years include:

- Alpine Investors’ $3.4 billion continuation fund for Apex Services Partners with capital support from Blackstone Strategic Capital, HarbourVest, Lexington Partners, and Pantheon

- KSL Capital Partners’ $3 billion continuation fund for Alterra Mountain Company, the largest heli-skiing company

The rise of continuation funds, which is a key part of the secondaries market as we will explain below, highlights a major shift in private equity. What’s more, traditional buyout firms like New Mountain, Warburg Pincus, and Leonard Green are now trying to launch their own continuation fund strategies.

History of Continuation Funds

Most readers are likely familiar with the traditional private equity structure, where limited partners (LPs) commit capital to general partners (GPs; i.e, PE firms), who then invest throughout the fund’s lifecycle, calling capital from LPs as needed.

On the other hand, continuation funds, which is a sub-category of secondaries, focus on purchasing existing LP interests, typically midway through a PE fund’s lifecycle. This strategy, first developed in the 1980s, gained traction following the Great Recession when liquidity dried up. In recent years, the secondary market has surged, offering PE firms a way to provide liquidity to existing LPs while maintaining ownership of their assets.

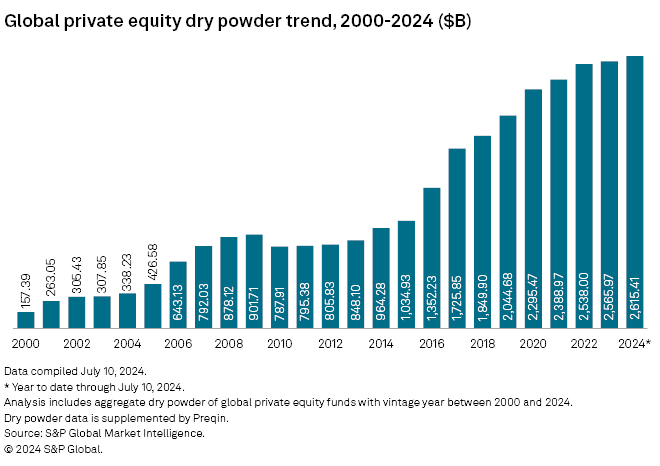

As the private equity landscape has grown increasingly competitive and deployment challenges mount—evidenced by record-high levels of dry powder in 2024—continuation funds have become an essential tool. By rolling over investments into these vehicles, GPs can extend their hold periods, sidestep traditional exit pressures, and maximize long-term value creation.

Source: S&P Global

👍 Why LPs invest in secondary markets

Larger LPs with in-house investment teams utilize the secondary market to actively manage their private equity exposure within their broader investment strategy. They can immediately increase exposure by purchasing secondary interests, rather than committing capital to PE funds and waiting for deployment.

Smaller LPs, on the other hand, typically participate by committing capital to secondary funds managed by firms like Blackstone Strategic Partners and HarbourVest Partners. These funds offer several key benefits:

Diversification: Secondary investments provide exposure to a broad range of assets across multiple strategies, sectors, vintage years, and geographies, helping to reduce overall portfolio risk.

Reduced Blind Pool Risk: Unlike primary PE investments, secondaries allow LPs to invest in known assets with established track records, offering greater transparency and risk mitigation.

Attractive Pricing: Secondary interests are often acquired at a discount to Net Asset Value (NAV), enhancing potential returns.

J-Curve Mitigation: Investing in mature assets allows LPs to bypass the early negative return phase typical of primary PE investments, leading to faster potential returns.

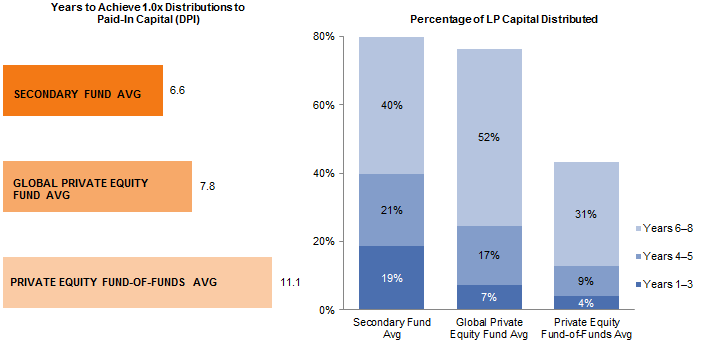

Because secondary funds purchase companies midway through the investment cycle, they tend to:

Return capital more quickly than traditional PE funds.

Front-load capital calls, which is preferred over end-of-life capital calls, as it makes cash flow planning more predictable.

Source: Cambridge Associates

✌️ Types of Secondary Transactions

Broadly speaking, there are two types of secondary transactions: LP-led and GP-led. GP-led secondaries can take different forms, including continuation fund structures or tender offers. The table below focuses on the continuation fund structure for GP-led secondaries.

Category | LP-Led Secondaries | GP-Led Secondaries |

Initiator | An individual LP selling its fund interest to another investor. | The GP transfers assets into a new vehicle (i.e., a continuation fund) to provide all LPs with an option to sell or roll over. |

Primary Motivation | The LP seeks liquidity or portfolio rebalancing. | The GP extends asset hold periods, while offering liquidity to existing LPs. |

Transaction Type | Sale of fund stakes by LPs, often involving interests across multiple funds/companies. | Transfer of one or more assets into new vehicles. Even for multi-asset deals, the assets typically come from the same fund. |

Buyer Focus | Buyers acquire diversified portfolios at a discount to NAV, minimizing blind pool risk. | Buyers gain access to concentrated assets with potential for further growth. |

Liquidity Options | LPs exit entirely by selling their stake. | Existing LPs can choose to cash out or roll over into the new vehicle. |

Structure of Continuation Funds

A typical continuation fund is structured as a separate, newly formed investment vehicle. This new fund is created specifically to acquire one or more assets from an existing private equity fund that is nearing the end of its term.

For example, in the structure chart below:

The Legacy Fund may hold multiple assets (e.g., Companies A, B, and C) and have multiple limited partners (LPs).

In a Continuation Fund, a subset of assets (e.g., Company A) is transferred to a new vehicle.

Each LP can elect to roll over their interest into the new fund or sell their stake.

Selling LPs receive cash from new investors in exchange for their interest.

The GP/PE firm maintains control of both the Legacy Fund and the Continuation Fund.

Source: NYU Journal of Law & Business

Economics of Continuation Funds

GPs have very compelling economic reasons to launch continuation funds:

Carry realization and rollover:

The GPs' carry in the transferred assets is realized and rolled into the continuation fund as equity. Typically, 100% of carry is rolled as equity to align economic interests with the new investors. This also allows GPs to defer taxes until the ultimate exit of the continuation fund.Resetting the investment lifecycle:

With a continuation fund, the investment lifecycle is reset, meaning GPs can continue to charge management fees to both new investors and rollover investors. If the assets had stayed in the legacy fund with an expired fund life (typically 10 years), GPs would stop receiving management fees. However, in the continuation fund, management fees tend to be lower than the typical 2%, and in some cases, even 0%.

Source: Paul Hastings

New carry pool:

A new carry pool is created, effectively allowing GPs to double dip on carry on the same asset. New investors and rollover investors agree to provide up to 20% carry to GPs to align incentives. However, unlike a typical PE fund carry of 20% above an 8% hurdle rate, continuation fund carry is often tiered at different MOIC hurdles.

Source: Paul Hastings

Tiered carry economics:

There’s a logical reason for tiered carry economics at different MOIC hurdles. Since the assets in a continuation fund are typically more mature in their investment lifecycle, they tend to be monetized earlier than the typical 5-7 year private equity hold. The shortened hold period, combined with the initial discount to NAV, tends to inflate IRRs even with a low MOIC. For example, historical data below shows secondary funds achieving an impressive 20.9% IRR, despite only a 1.39x MOIC.

Source: Cambridge Associates

Looking Ahead

It is without question that continuation funds have become an integral part of private equity. However, limited partners remain confused and frustrated by this new innovation. Will this hinder the growth of the continuation fund market? Or will LPs continue to play along, or even help GPs like New Mountain and Warburg Pincus raise their own secondaries funds?

That’s a wrap for the first edition of Training Tuesday. Let me know how you liked it using the poll below and see you Saturday with another Deep Dive!

Which Tuesday content do you prefer? |

RATE TODAY’S EDITIONWhat’d you think of today’s edition? |

If you enjoyed the newsletter, please share with friends and subscribe at https://perollup.beehiiv.com/subscribe

Reply